Vori x Progressive Grocer: The 2026 State of Independent Grocery

Jesse Lopez

Head of Product Marketing

·

June 15, 2026

·

8

min read

Vori commissioned EnsembleIQ, in partnership with Progressive Grocer, to survey independent grocery operators across the country — owners, general managers, and store managers with direct involvement in technology decisions. What we wanted was an honest read on where independent grocery stands heading into 2026: what's working, what's broken, and where the real opportunities are hiding.

The picture that came back is not grim. Independent grocery is not losing. But it is under sustained pressure from costs, competition, and operational complexity. The stores handling that pressure well are pulling visibly ahead of the ones that aren't.

This report covers what the data shows across three areas where the gap between those stores is widest: margins, labor, and sales.

State of the Industry: The Segment Isn't Losing, But a Gap Is Opening

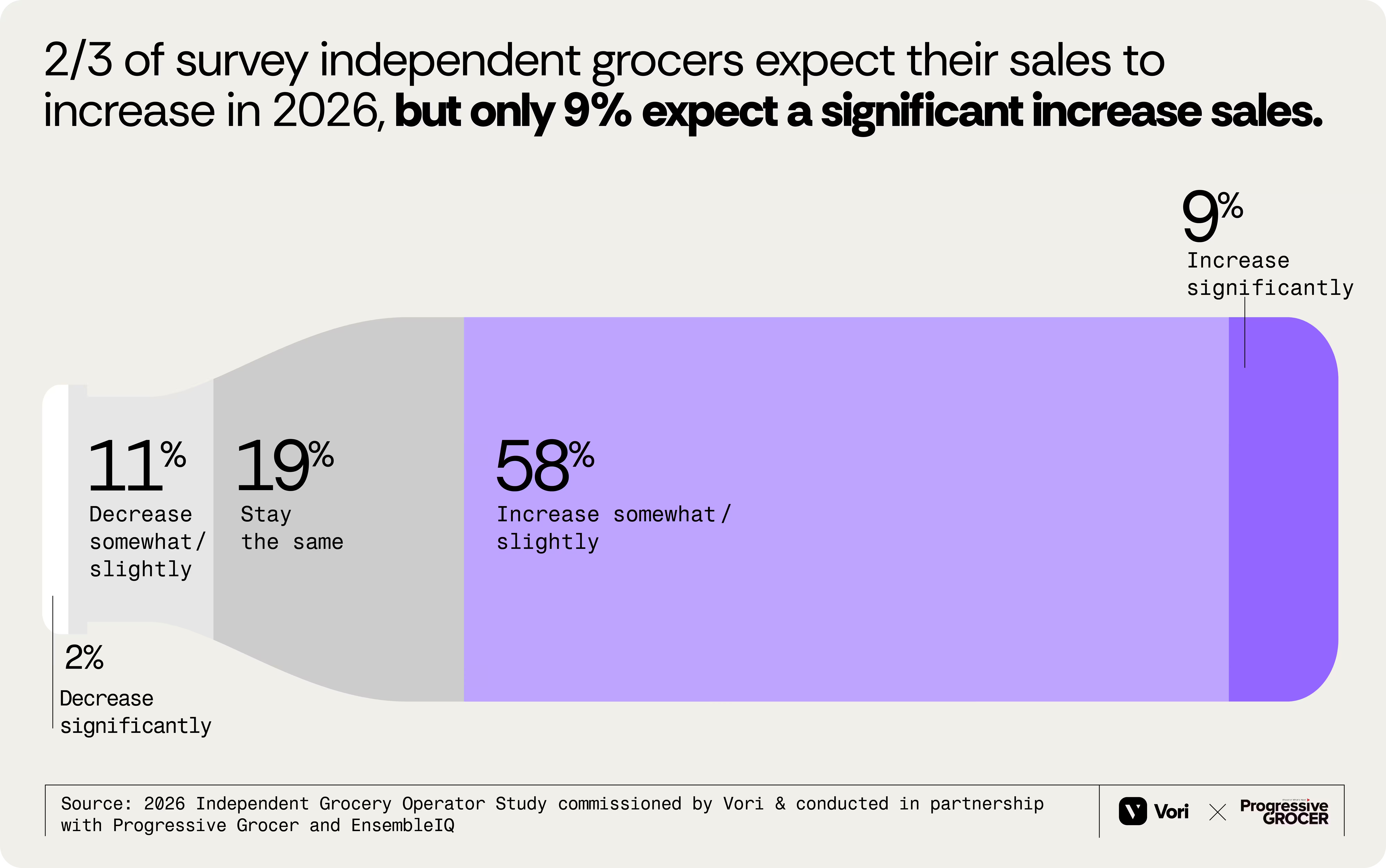

Let’s start with what operators told us about their own outlook. 67% expect their sales to increase in 2026. That's a meaningful number — it says this segment has genuine momentum, and that the operators running these stores believe in their position.

But only 9% expect significant growth. The majority are forecasting modest, incremental gains. In a business running on 1–3% margins, with vendor costs rising and labor getting more expensive, modest growth isn't a comfortable place to operate from. It's a position that rewards tight operations and leaves little room for error.

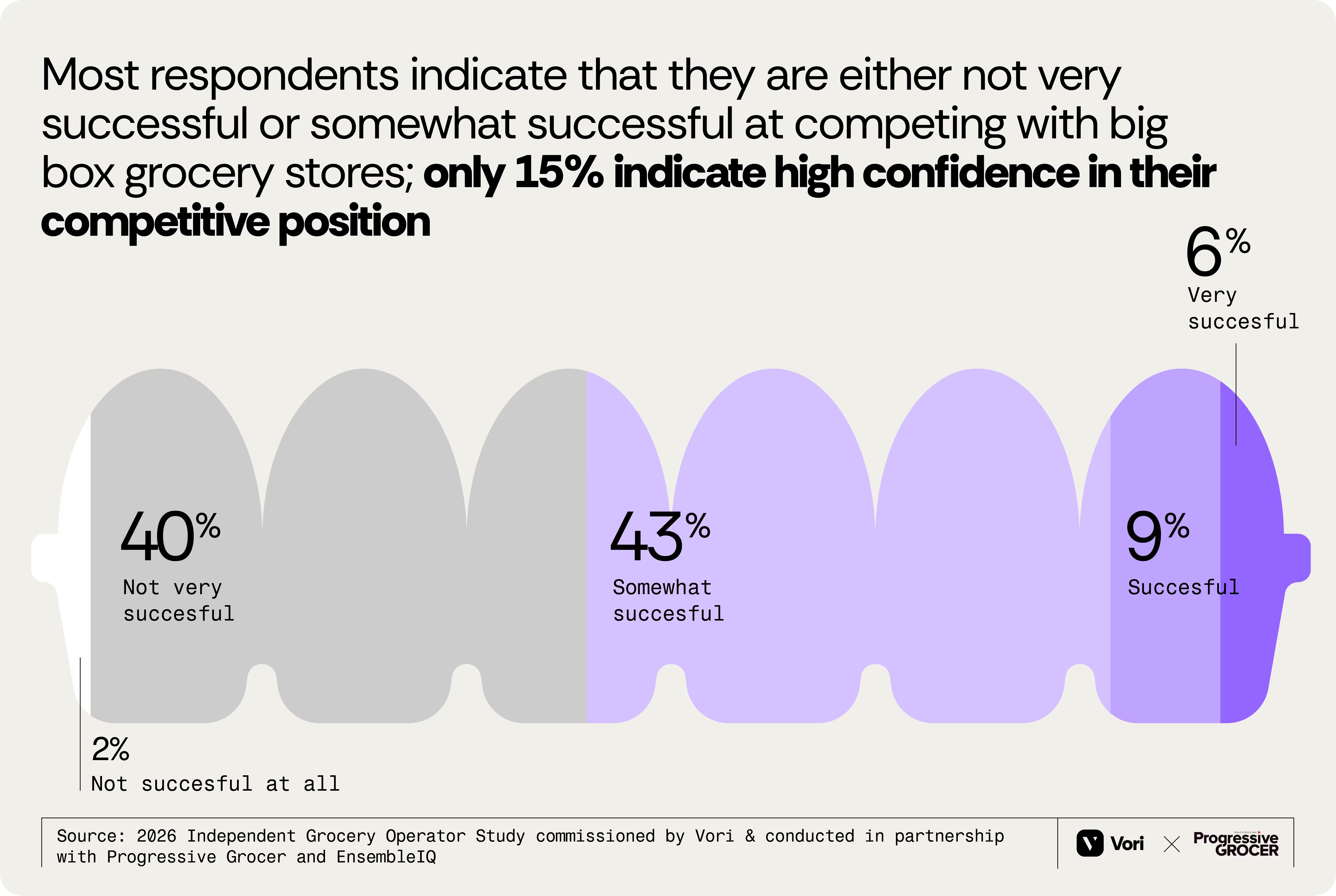

Most independent grocers do not feel like they’re winning against big box.

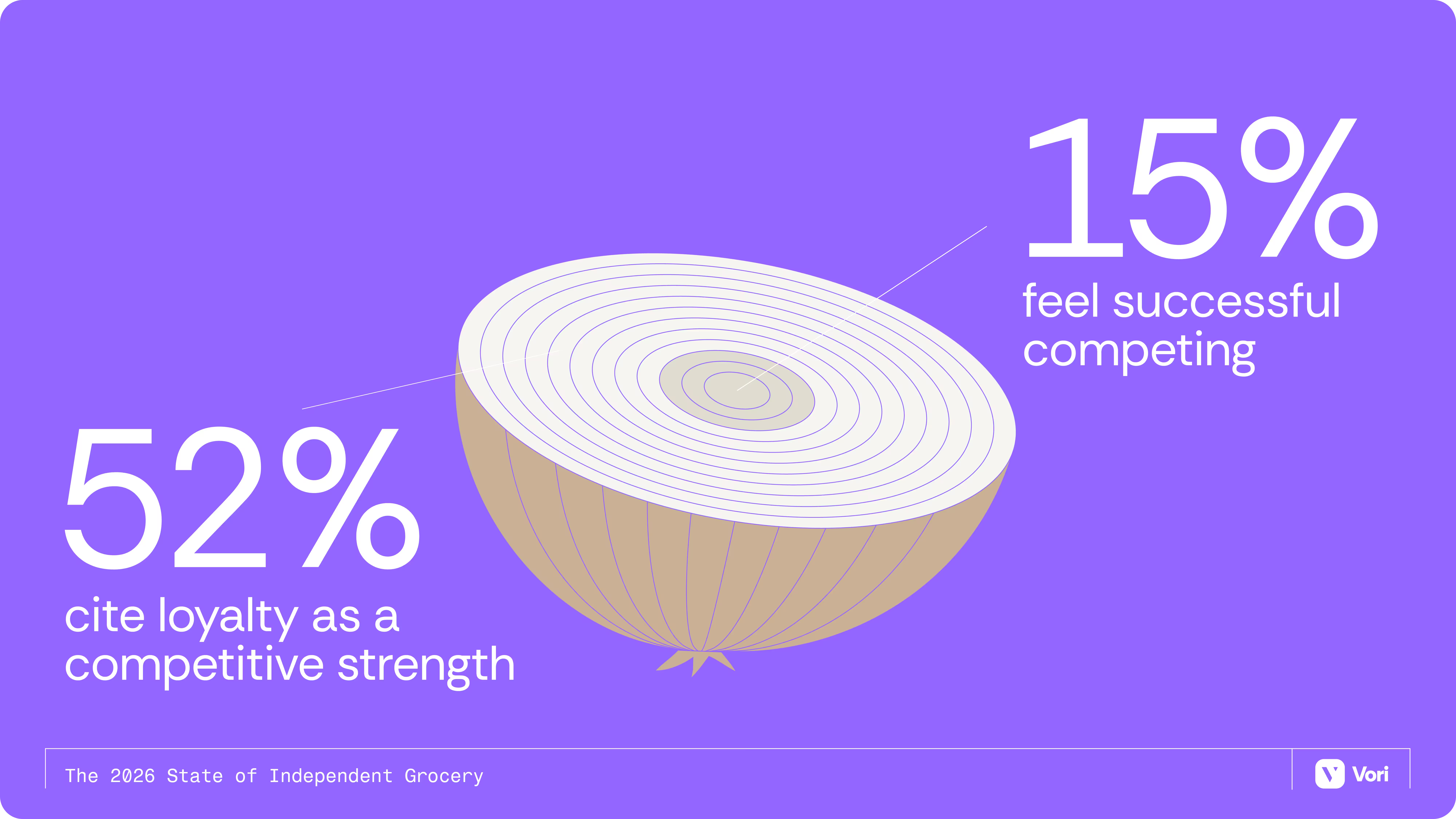

When we asked operators how successful they feel competing directly with big-box grocery, only 15% said they feel "successful" or "very successful." That's not a failure of ambition. Direct head-to-head competition with national chains on price and scale isn't where independent grocery wins. It isn't built to.

Independent grocery wins where the national chains can't follow.

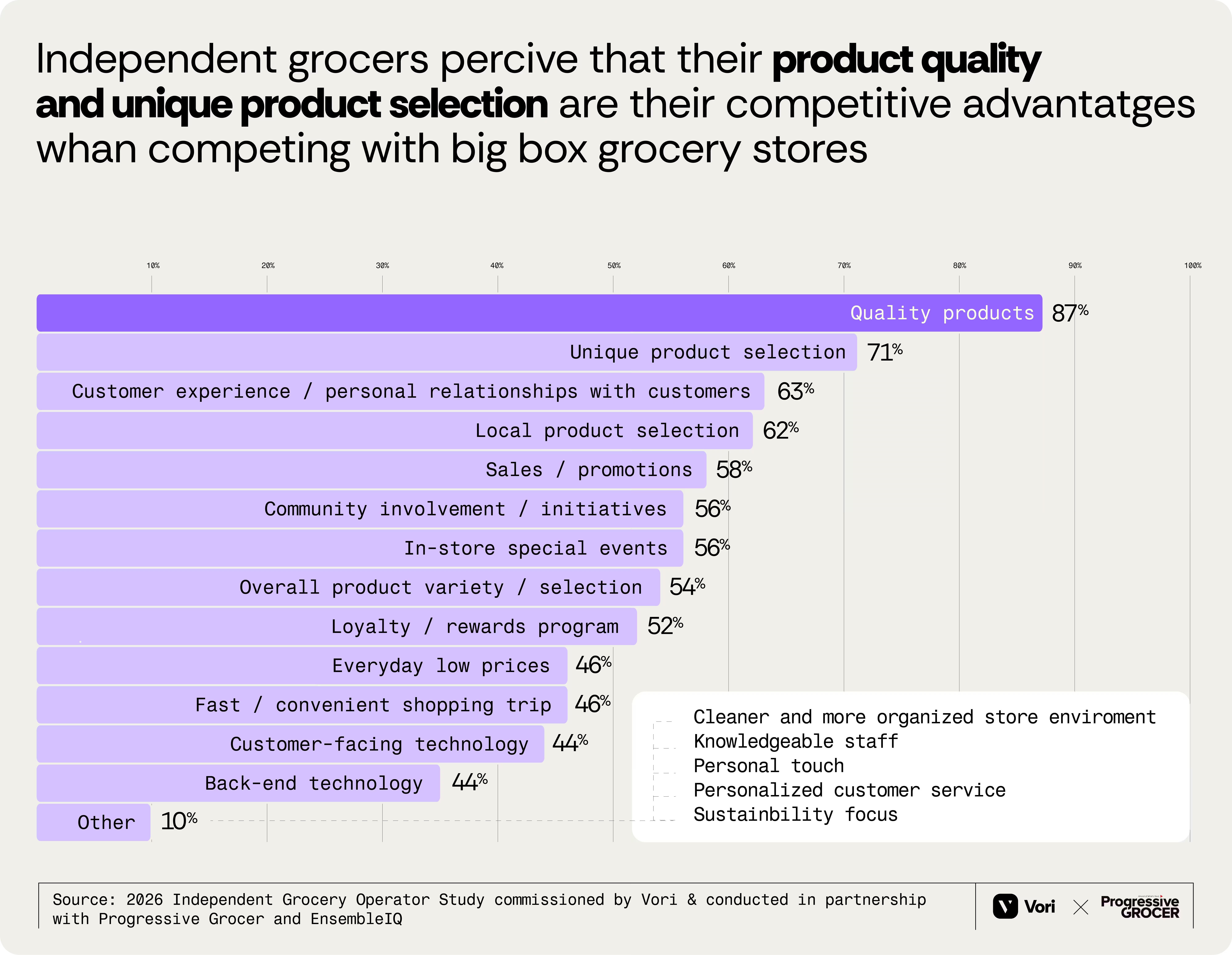

Where independents thrive — and where 87% of operators in this study say they have a genuine advantage — is product selection and customer service. When asked about key strengths independent grocers need to effectively compete against big box retailers, 71% point to unique product selection. 63% cite customer relationships and personal service. 62% name local product selection. 52% say loyalty and rewards programs.

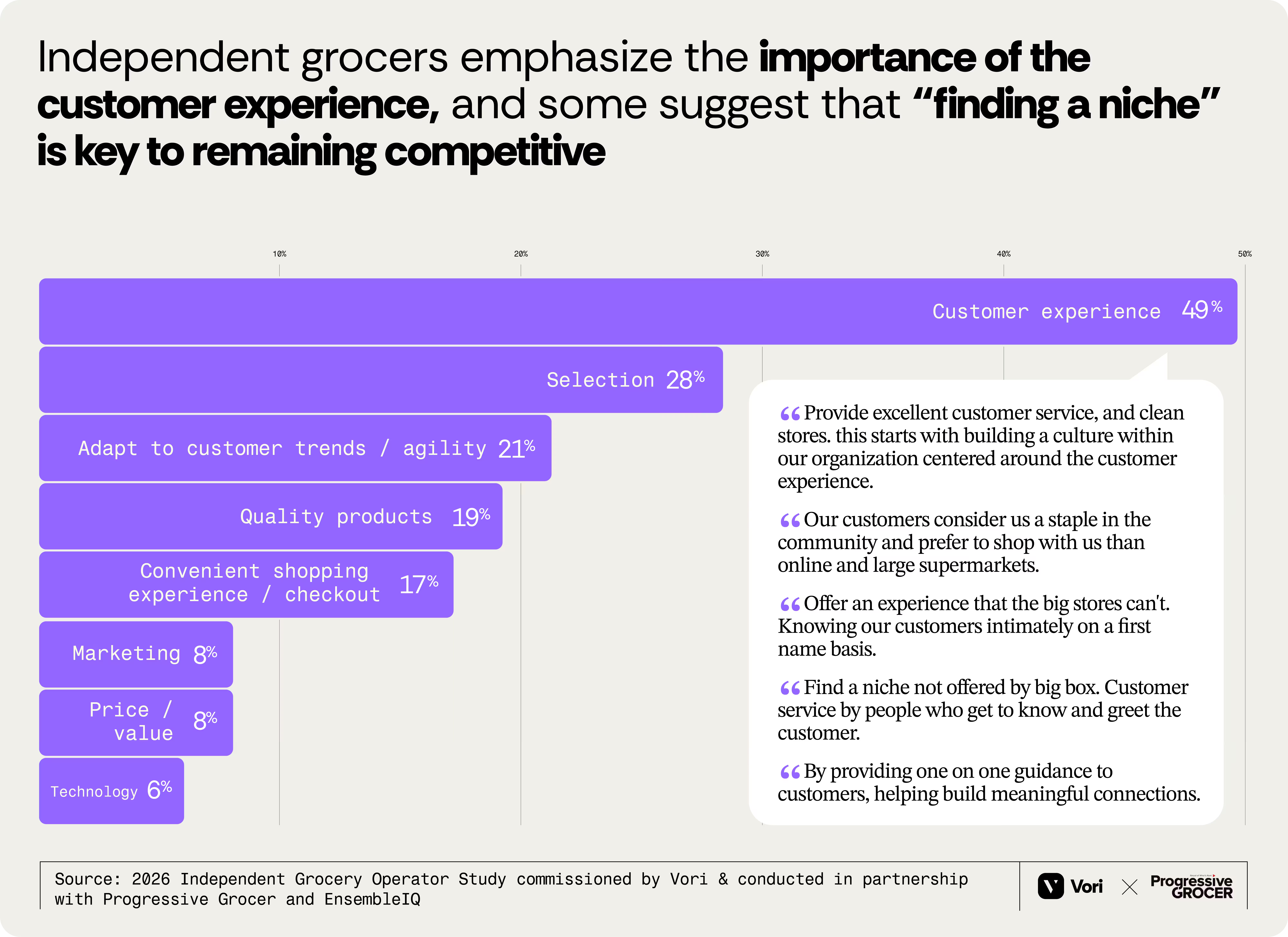

These are real differentiators. A neighborhood grocer that stocks local farms, knows regulars by name, and carries the specialty items the nearby Kroger never will — that local store has something a national chain with 200,000 square feet genuinely cannot replicate. When we asked operators what independents need to do to win against big-box, customer experience ranked first at 49%, followed by product selection at 28%. Price was 8%.

The operators who are growing have largely accepted this. They're not trying to compete on every dimension. They've carved out a niche — local, specialty, international, artisanal, or just deeply community-embedded — and they're building their operations around it. The challenge is operational discipline: the right products on the shelf, the right prices, the right customer relationships. That discipline is harder to maintain when the back office is running on manual processes and disconnected systems.

"What you see in independents is a connection to the food supply chain that could never scale for a national retailer."

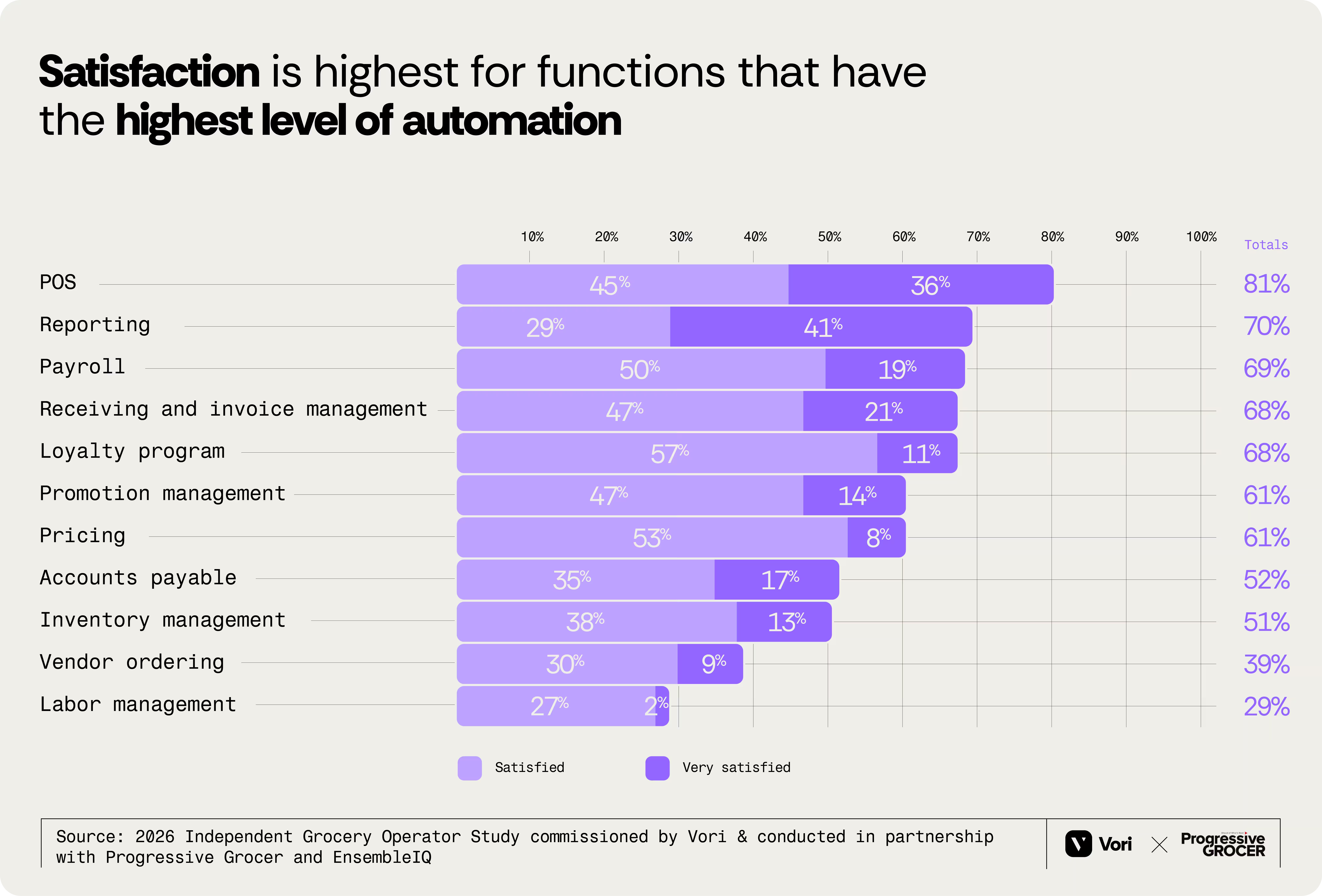

Higher automation means higher satisfaction — in every function, without exception.

The survey tracked automation levels and satisfaction scores across eleven core operational functions, from POS to loyalty to vendor ordering. The pattern is consistent across all of them: the stores running more automated systems are more satisfied with how their operations run, across margins, labor, and sales. Every single function. No exceptions.

The inverse is equally true. The two functions with the lowest automation — labor management at 13% mostly or fully automated, vendor ordering at 34% — also report the lowest satisfaction of any category in the study. The manual work isn't just slow. It's wearing people down.

Most operators know AI can help. Most aren't using it yet.

The awareness is there. When asked which areas of their stores would benefit most from AI and automation tools, operators named promotion management (68%), reporting (68%), pricing (64%), POS (60%), and inventory management (60%). These are the daily operational tasks consuming the most time and generating the most frustration.

But knowing and doing are different things. Only 13% of operators are currently using AI or automation tools in a meaningful way, but 70% of operators are either planning to adopt or exploring (34% are planning to adopt and 36% are exploring with no firm timeline). The interest is there for the vast majority of operators which correlates to the previous section on automation being positively correlated with satisfaction. But the stores already in the 13% actively using AI or automation tools are building operational advantages that compound — better demand forecasting, smarter pricing decisions, less time spent on tasks that don't require a person. The stores waiting are watching that gap widen.

The hesitation is understandable. New tools carry implementation risk, training burden, and cost. But the survey data makes the cost of staying manual equally visible: the functions where automation is lowest are precisely the functions where operators are least satisfied and spending the most hours per week. That's not a coincidence. Additionally, the cost of inaction will continue to increase as the world changes and more and more independent grocers adopt AI. The time to get ahead is now.

Challenges: Where Margin, Hours, and Loyalty Slip Away

When asked about their biggest concerns for the year, the list independent grocers returned is long — and it spans every part of the business. Operational costs topped the chart at 83%, followed closely by competition from big-box grocery at 77%, cost of labor at 74%, and inventory management at 68%. Further down: supply chain disruptions (64%), margin pressure from price competitiveness (60%), finding quality talent (58%), and keeping up with the pace of change in technology (45%).

When operators were asked to pick their single #1 challenge — not a list, just one — the answers sharpened considerably:

- 23% said operational costs

- 17% said competition from big-box grocery competitors

- 17% said pressure on margins from price competitiveness

- 13% said inventory management

What that forced ranking reveals is where the real weight sits. Operational costs and margin pressure aren't just common concerns — they're the ones keeping owners up at night. And notably, big-box competition and margin pressure tie for second place, which isn't a coincidence. For most independent grocers, those two pressures are the same problem showing up in different places: big-box drives down the prices customers expect, which compresses the margin independent operators can actually charge.

These pressures aren't new. What is new — or at least newly visible — is the degree to which technology is determining who handles these challenges well and who doesn't.

Before getting into each challenge, one finding sets the context for all of them:

- ⅓ of operators say their POS is only "somewhat integrated" or "not well integrated" with their other technology tools

- ⅓ say they don't use back-office software at all.

A fragmented or absent technology foundation doesn't just create inefficiency — it means that good decisions made in one system don't propagate to the rest of the business. A price change approved somewhere doesn't automatically update the shelf tag. A cost increase caught on an invoice doesn't automatically flag a pricing review. Every gap in the stack is a gap in visibility, and visibility is what separates stores that manage their margins, labor, and sales proactively from stores that find out what happened after the fact.

Those gaps are visible from the outside too. UNFI, one of the country's largest distributors to independent grocery, sees how these operational pressures play out across its customer base.

"Independent grocers no longer have the luxury of being average."

Margins are eroding in ways most stores can't see in real time.

Forty-three percent of operators named margin management as their single most important operational focus for the year. It ranked first above every other priority — above price change management, labor efficiency, loyalty, all of it.

Grocery margins don't leave room for error. It’s a penny margin business. When a vendor raises a cost on a DSD invoice and no one catches it before the product hits the shelf, that item sells at the wrong margin until someone happens to notice. In a store running thousands of SKUs across dozens of vendors, with deliveries arriving throughout the week, undetected cost changes are a recurring tax on profitability that never shows up as a line item.

49% of operators said they don't have a reliable system to catch vendor cost changes when they happen. 55% named price change management as a capability they need to improve. These aren't operators who don't care about margin. The problem is structural: when the system doesn't surface the information fast enough, caring doesn't close the gap.

Nick, owner of The Willows Market in Menlo Park, found out after the fact that he'd been selling a chocolate bar for $3.99 when he was paying $4.70 for it. No alert, no flag — just a margin leak compounding for however long the item sat at the wrong price. Before switching systems, printing a single price shelf tag was a 30-minute process. Price changes were inconsistent across the store. The margin conversation was always happening after the damage was done.

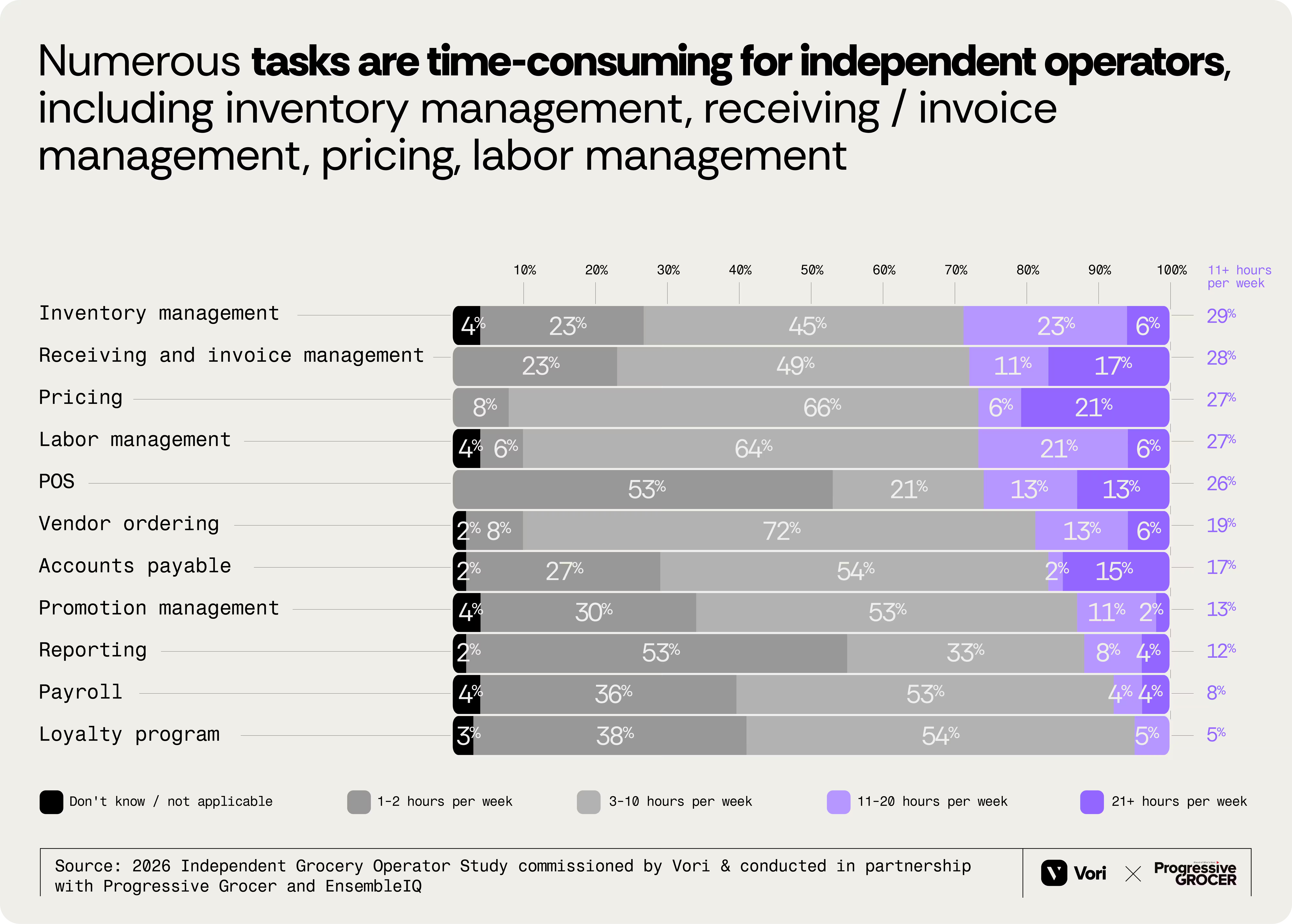

Back-office work is consuming hours that should go toward the floor.

Independent grocers are spending dozens of hours per week on manual back office activities. Inventory management runs eleven-plus hours per week for 29% of operators — and 36% named it the area where they most need better technology. Receiving and invoice management consumes that same eleven-plus hours for 28%. Vendor ordering, still done largely from memory and clipboards at most stores, sits among the most time-consuming and least satisfying processes in the building.

The cost of all this manual work doesn't appear cleanly on a P&L. An operations director spending three hours building a produce order from memory on a Sunday afternoon isn't showing up as waste anywhere on the financial statements. But those hours have real costs — in labor, in accuracy, and in what doesn't get done while someone is doing paperwork.

"This technology has the potential to unlock unprecedented efficiency and abundance for independents across the industry."

The survey's automation-satisfaction correlation makes this concrete. Across all eleven functions tracked, the functions with higher automation consistently show higher satisfaction. Not sometimes — every time. When the system handles the repeatable work, people are less frustrated, errors go down, and the hours come back. When they're doing it manually, the satisfaction scores reflect exactly what you'd expect.

Regional wholesalers see this firsthand. The operational friction created by manual receiving, paper invoices, and disconnected ordering doesn't just affect the store — it flows downstream to the distributor relationship too. Ira Higdon, a regional wholesaler that has spent decades supplying independent grocers across the Southeast, describes what manual back-office operations look like from the other side of the delivery dock.

" I am told the error rate with vendors is at an all time high, and the time it takes to check in vendors and catch costing errors takes retailers away from their other day to day duties."

Most loyalty programs aren't changing customer behavior yet.

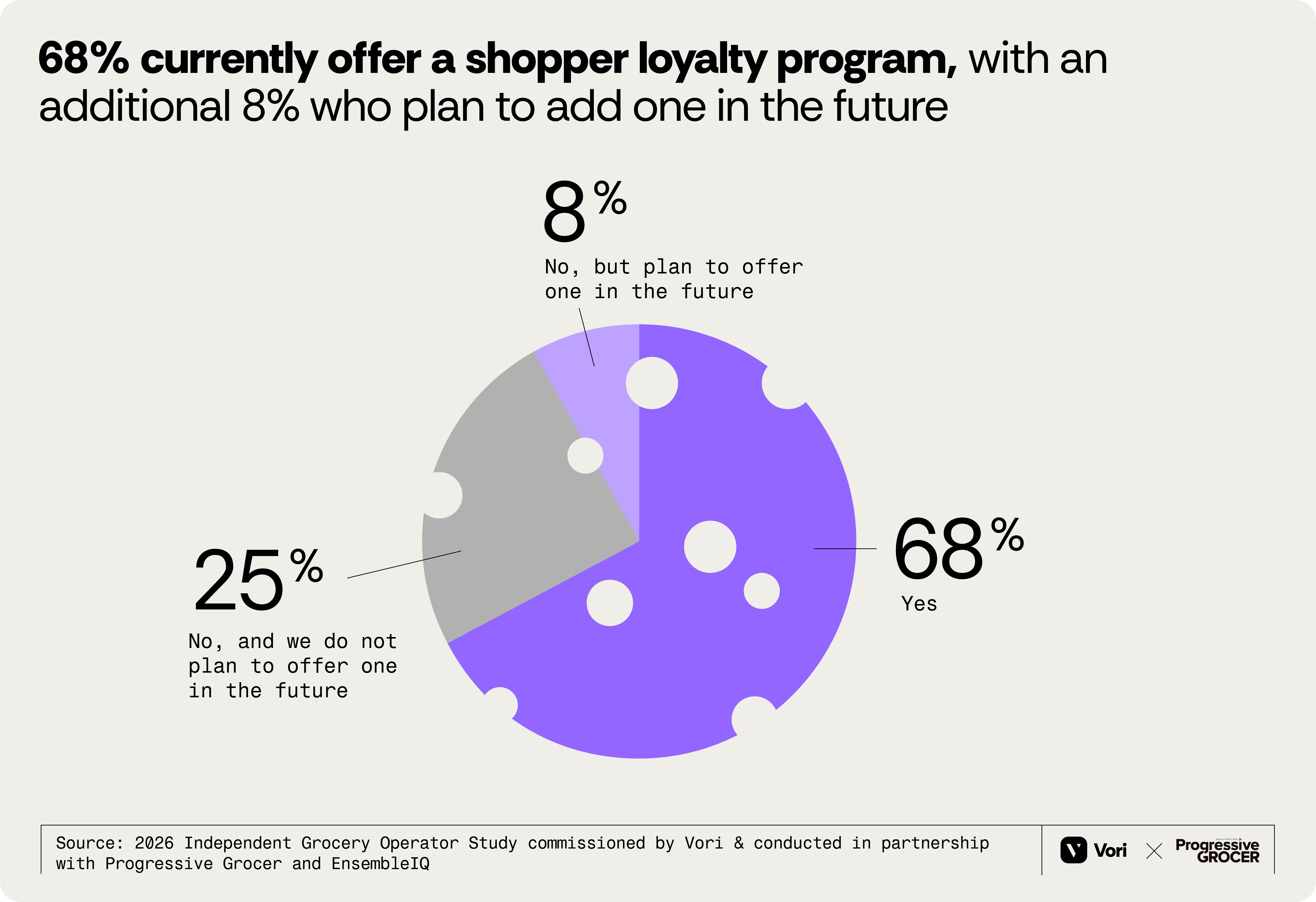

68% of independent operators run a shopper loyalty program. That number reflects something real about how independent grocers think about their customers. These are stores built on personal relationships — and operators are investing in tools to formalize and extend those relationships at scale. For a segment often characterized as slow to adopt new tools, 68% is genuinely higher than expected — and it reflects something real about how seriously independent grocers take the relationship with their customers.

The harder question is whether those programs are working.

Of operators with a loyalty program, only 42% use purchase history to personalize offers. Only 17% make personalized product recommendations based on what customers have bought. Nearly half report difficulty integrating their loyalty platform with their POS.

A loyalty program that gives the same discount to every customer regardless of behavior isn't changing behavior — it's discounting transactions that would have happened anyway. The whole premise of loyalty is getting customers to visit more often, spend more per trip, and reward shoppers for choosing your store over the alternatives. That requires knowing who your customers are and reaching them with something relevant to them specifically.

What makes this data particularly pointed: 52% of operators cited their loyalty program as a competitive strength against big-box grocery, but in the same survey, only 15% said they feel "successful" or "very successful" competing with big-box.

Loyalty is being claimed as a strength. The programs most operators are running aren't yet delivering the outcomes that make it one — largely because they aren't connected to the POS and aren't built around purchase behavior.

Opportunities: Where the Growing Stores Win Them Back

Each of the challenges above has a corresponding opportunity. In every case, the stores that have already moved on it are showing concretely what's possible — in their margins, in the hours they've gotten back, and in what their customers are doing.

Personalized loyalty is how independents win the customer relationship — and the sales line.

One of the consistent findings is that independent grocers believe their relationship with customers is their most defensible competitive advantage. 63% named customer experience and personal relationships as a key strength against big-box. 49% said customer experience is what independents need to prioritize to win.

Loyalty technology, done right, is what scales that relationship. A well-run program doesn't replace the human connection — it reinforces it. When a customer gets an offer for the exact product they buy every week, that's a store that knows them. When they accumulate points and come back to redeem them, that's a relationship with a reason to continue.

The stores making loyalty work share the same fundamentals. Enrollment happens at the register by phone number in under a minute — no app download, no separate sign-up, no friction that lets the moment pass. Offers go out by SMS, timed to drive a specific visit, built from what customers actually buy. Operators track basket lift between members and non-members so they can tell whether the program is changing behavior or just discounting people who were already coming in.

Derek, owner of Valley Farm Market in Spring Valley, California, describes what it looks like when it's working: customers telling him they're saving their points, coming back specifically to use them, tracking their balance. "I ask 'Do you want to use your points?' and they say 'Nope, I am going to save those.' I am just excited that they are excited to come back and spend more money."

For the 32% of operators without any loyalty program and the many more running one that isn't connected to their POS, the path to more sales doesn't require finding new customers. It starts with the ones already walking through the door.

Digitize ordering, receiving, and inventory. Get the hours back.

The survey identifies inventory management, receiving and invoice management, and vendor ordering as the three functions with the highest demand for better technology and the lowest current satisfaction. These also happen to be the functions that are eating the most hours per week.

That's where the ROI on better tooling is most immediate and most concrete. When a produce order takes 45 minutes instead of three hours, that's two-plus hours a week that goes back to the store. When invoices get verified at the dock instead of reconciled from paper two days later, errors get caught while there's still a driver to call. When cost changes surface automatically on every incoming invoice, the margin conversation happens before the product hits the shelf at the wrong price — not after.

Victor, Director of Operations of Talin Market, Albuquerque, New Mexico describes how he has cut ordering times down: “I used to do my own consolidation of movement data for our large produce orders, and that used to take me a good 2 to 3 hours to do… now it can be done in less than an hour.”

But the more important point is what those recovered hours make possible. The reason independent grocers have strong customer relationships and deep community ties isn't accidental. It's the result of operators and their teams spending time on the floor, with customers, learning what the neighborhood needs. Every hour recovered from manual back-office work is an hour that can go back to the thing that actually differentiates these stores.

Technology doesn't replace that. It protects the time for it.

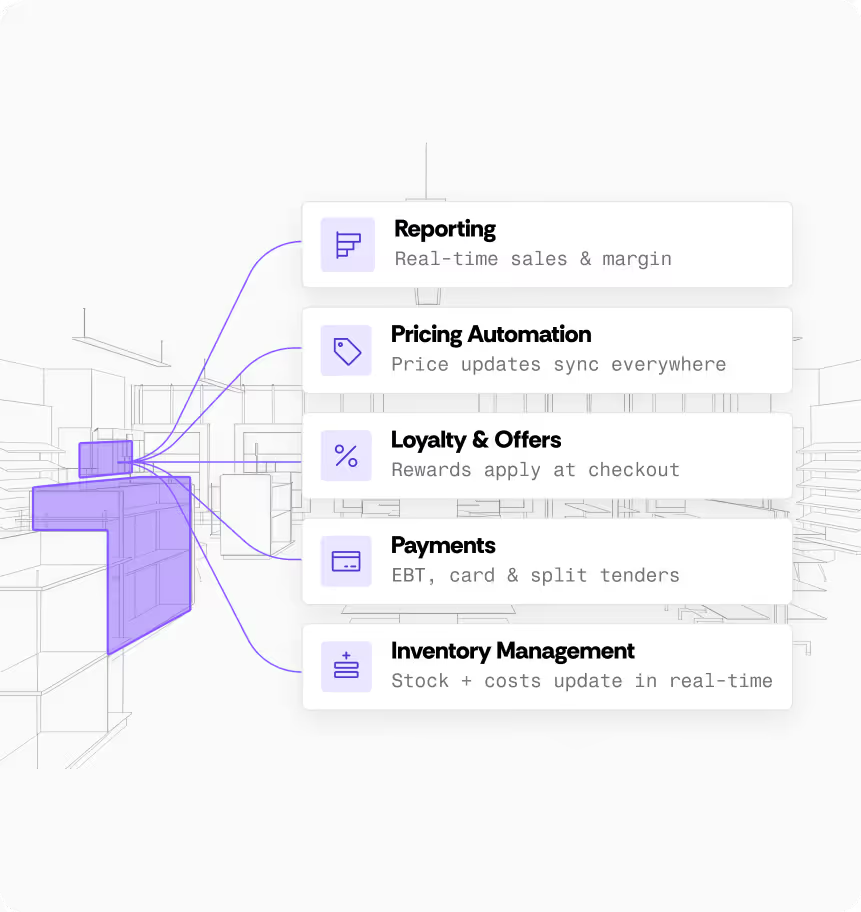

Run checkout, pricing, ordering, and loyalty on one system.

A large part of why the challenges above persist is that most independent stores are running on disconnected tools. Pricing in one system, inventory in another, loyalty on a separate platform that doesn't talk to the POS, ordering on a spreadsheet or a clipboard. Each system works in isolation. None of them talk to each other.

The practical cost: a price change approved in the back office doesn't automatically update the shelf tag or the POS. A vendor cost increase caught on an invoice doesn't automatically trigger a pricing review. Loyalty enrollment requires a separate step that the cashier may or may not take. The operator ends up bridging all these gaps manually — which is exactly the work consuming so many hours per week.

When POS, ordering, inventory, pricing automation, and loyalty run as one connected system, those gaps close. A cost change on an invoice surfaces as a pricing flag at the same time as the receiving confirmation. A promotion built in the back office flows to checkout automatically. Loyalty enrollment happens at the point of purchase without a separate workflow. Reporting pulls from a single source of truth rather than from five different systems that have to be reconciled.

This kind of integration isn't a distant aspiration for independent grocery. It's available now, at a cost that makes sense for a single-location or small-chain operator. The stores already running on connected systems aren't just more efficient — they have visibility into their business that operators on fragmented stacks simply don't have. They see the margin impact of a vendor cost change the day it happens. They know which loyalty members are at risk of lapsing before they're already gone. They can make a pricing decision based on real data in the time it used to take to pull a report.

Independent grocery stores that win in 2026 won't look different from the outside. They'll still know their customers by name. They'll still carry products the nearby chain doesn't stock. They'll still be the store people drive past three alternatives to reach. What will be different is what's running underneath — systems that protect the margin on every item, give the team back hours that used to go to paperwork, and keep the customers coming back with intention rather than habit.

That is the combination for grocers who play to win.

About Vori

Vori is the modern grocery operating system built for independent grocers — connecting checkout, pricing, ordering, receiving, loyalty, and reporting in one place, built from scratch for how grocery actually works.

→ Book a demo at vori.com or call (650) 651-5058.

Survey Methodology

Vori commissioned the 2026 Independent Grocery Operator Study to benchmark the state of independent grocery across current and future outlooks, sentiment regarding big box competitors, and grocery technology and loyalty programs. The survey was conducted in partnership with Progressive Grocer and EnsembleIQ’s research department with the resulting findings prepared by the EnsembleIQ research team.The survey fielded from January 28, 2026 – February 26, 2026 and responses were gathered from n=53 respondents (50 responses is industry standard for B2B surveys with a unique audience profile). Respondents were screened to ensure that they had the following qualifications:

• Employed at a grocery retailer in the United States

• General Manager / Store Manager or above role

• 1-10 store locations

• Involvement in or authority on technology business decisions

Note: due to rounding, questions where data should sum to 100% may differ +/- one percentage point (e.g. may total 99% or 101% instead of 100%).

FAQs

Everything you need to know about Vori. Can’t find the answer you’re looking for? Please chat to our friendly team.

You may also like

POS, Pricing, Inventory, Loyalty: Why Your Grocery Tools Need to Share the Same Data

Learn why the problem isn't your grocery tools but the gaps between them. When POS, pricing, inventory, and loyalty don't share data, you lose margin you can't see. Here's what connecting them changes.

POS, Pricing, Inventory, Loyalty: Why Your Grocery Tools Need to Share the Same Data

Learn why the problem isn't your grocery tools but the gaps between them. When POS, pricing, inventory, and loyalty don't share data, you lose margin you can't see. Here's what connecting them changes.

Explained

The Complete Guide to Grocery Store Management Software in 2026 (Features That Actually Matter)

Most grocery store management software is built for general retail, not grocery. Here are the capabilities that actually matter for independent stores, and why they only pay off when they connect.

The Complete Guide to Grocery Store Management Software in 2026 (Features That Actually Matter)

Most grocery store management software is built for general retail, not grocery. Here are the capabilities that actually matter for independent stores, and why they only pay off when they connect.

Buyer's Guide